Iran-US Ceasefire Fragility Shifts Market Focus Back to Inflation and Interest Rates

The fragile truce between the United States and Iran, teetering on the brink of collapse, has reintroduced inflation as the dominant concern for global bond markets, reinforcing expectations that central banks will maintain elevated interest rates for an extended period. This geopolitical shift comes as investors grapple with the dual pressures of escalating Middle East tensions and the persistent specter of inflationary pressures in major economies.

The ceasefire, brokered amid months of diplomatic efforts to ease hostilities, has been thrown into uncertainty following recent provocations and unresolved conflicts in the region. While the initial agreement provided a temporary reprieve from geopolitical risks, its fragility has reignited fears of energy price volatility and supply chain disruptions. As a result, bond markets are recalibrating their focus toward inflation dynamics, with traders increasingly pricing in the likelihood that interest rates will remain higher for longer than previously anticipated.

The Geopolitical Context: Iran-US Tensions and Market Implications

The relationship between the United States and Iran has long been a flashpoint for global markets. Historical tensions, including sanctions, nuclear program disputes, and military confrontations, have frequently driven fluctuations in oil prices and investor sentiment. The recent ceasefire, though hailed as a tentative step toward stability, has been undermined by ongoing disagreements and regional instability.

Iran’s continued support for proxy groups in conflict zones and its nuclear ambitions have sparked renewed friction with Washington. Meanwhile, U.S. sanctions remain a contentious issue, stalling diplomatic progress and leaving the ceasefire on shaky ground. This precarious situation has reintroduced geopolitical risk into financial markets, with oil prices edging higher amid fears of potential disruptions to Middle Eastern energy supplies.

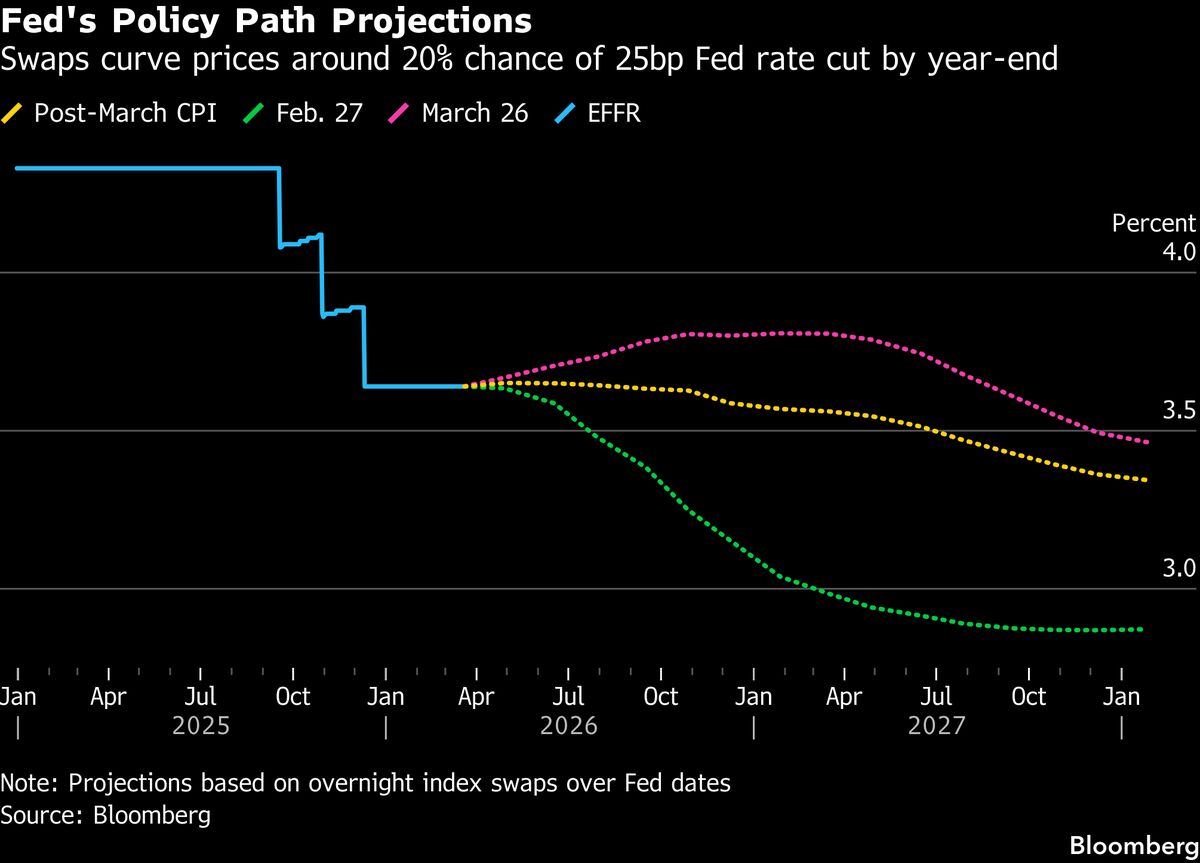

The impact on global markets has been swift and pronounced. Bond yields, which move inversely to prices, have climbed as investors recalibrate their expectations for inflation and central bank policy. The yield on the benchmark 10-year U.S. Treasury note, a key indicator of market sentiment, has surged to multi-month highs, reflecting concerns that persistent inflationary pressures will delay rate cuts.

Inflation and Interest Rates: The Central Bank Dilemma

The resurgence of inflation concerns comes at a critical juncture for central banks worldwide. After aggressively raising interest rates in 2022 and 2023 to combat soaring inflation, policymakers in the U.S., Europe, and other major economies have signaled a cautious approach to easing monetary policy.

In the United States, the Federal Reserve has emphasized its commitment to achieving its 2% inflation target, even as economic growth shows signs of moderation. Recent data has indicated that core inflation remains stubbornly elevated, driven by rising service costs and tight labor market conditions. The fragility of the Iran-US ceasefire has added another layer of complexity, with potential energy price spikes threatening to reignite broader inflationary pressures.

Similarly, the European Central Bank (ECB) faces a delicate balancing act. While inflation in the Eurozone has eased from its peak, underlying price pressures persist, particularly in the services sector. Geopolitical risks, coupled with structural challenges such as supply chain bottlenecks and wage growth, have led ECB officials to adopt a hawkish stance, suggesting that rate cuts may be delayed until later in the year.

In Asia, central banks are grappling with similar issues. China’s patchy economic recovery has complicated the inflation outlook, while Japan’s decades-long battle with deflation appears to be turning a corner, prompting speculation about potential policy shifts by the Bank of Japan.

Market Reactions and Investor Sentiment

The shifting focus back to inflation has sparked a wave of volatility across financial markets. Equities have faced headwinds as rising bond yields weigh on valuations, particularly in the technology sector, which is highly sensitive to interest rate movements. Meanwhile, commodities such as oil and gold have experienced upward pressure, reflecting both geopolitical risk and inflationary hedging by investors.

In the bond market, the sell-off has been broad-based, affecting government debt across major economies. U.S. Treasuries, German Bunds, and UK Gilts have all seen yields rise as investors reassess the trajectory of interest rates. The yield curve, a key indicator of economic expectations, has steepened, signaling concerns about the sustainability of economic growth amid tighter monetary conditions.

Corporate bond markets have also felt the impact, with spreads widening as risk appetite diminishes. Companies reliant on borrowing face higher financing costs, potentially dampening investment and economic activity.

The Broader Economic Outlook

The renewed focus on inflation and interest rates underscores the challenges facing global policymakers as they navigate a complex and uncertain economic landscape. While the immediate impact of the Iran-US ceasefire fragility may be felt in energy markets and investor sentiment, the broader implications extend to growth, labor markets, and consumer spending.

In the United States, robust job creation and resilient consumer demand have supported economic momentum, but higher borrowing costs and tighter credit conditions pose risks to future growth. Similarly, in Europe, the ECB’s restrictive monetary policy has weighed on economic activity, particularly in interest-rate-sensitive sectors such as housing and manufacturing.

Emerging markets face their own set of challenges. Elevated U.S. Treasury yields have strengthened the dollar, increasing the cost of servicing dollar-denominated debt and exerting pressure on currencies. For countries dependent on energy imports, rising oil prices could exacerbate inflation and strain economic stability.

A Delicate Balancing Act

As the Iran-US ceasefire hangs in the balance, global markets are once again reminded of the interconnectedness of geopolitics and economics. While the immediate focus has shifted back to inflation and interest rates, the broader narrative underscores the delicate balancing act facing policymakers and investors alike.

In the coming months, the trajectory of bond yields, central bank policy, and inflation will hinge on a confluence of factors, from geopolitical developments to economic data trends. For now, the message from markets is clear: the era of low interest rates is firmly in the rearview mirror, and uncertainty remains the prevailing theme. As one analyst aptly noted, “In a world of shifting sands, the only certainty is volatility.”