China Tightens Monetary Policy as Central Bank Cuts Medium-Term Lending

Beijing takes measured steps to curb excess liquidity amid economic recalibration

Beijing, [Date] – China’s central bank has moved to tighten liquidity conditions in the financial system by scaling back medium-term lending to commercial banks, signaling a cautious approach to managing monetary policy as the world’s second-largest economy navigates uneven growth and financial stability risks.

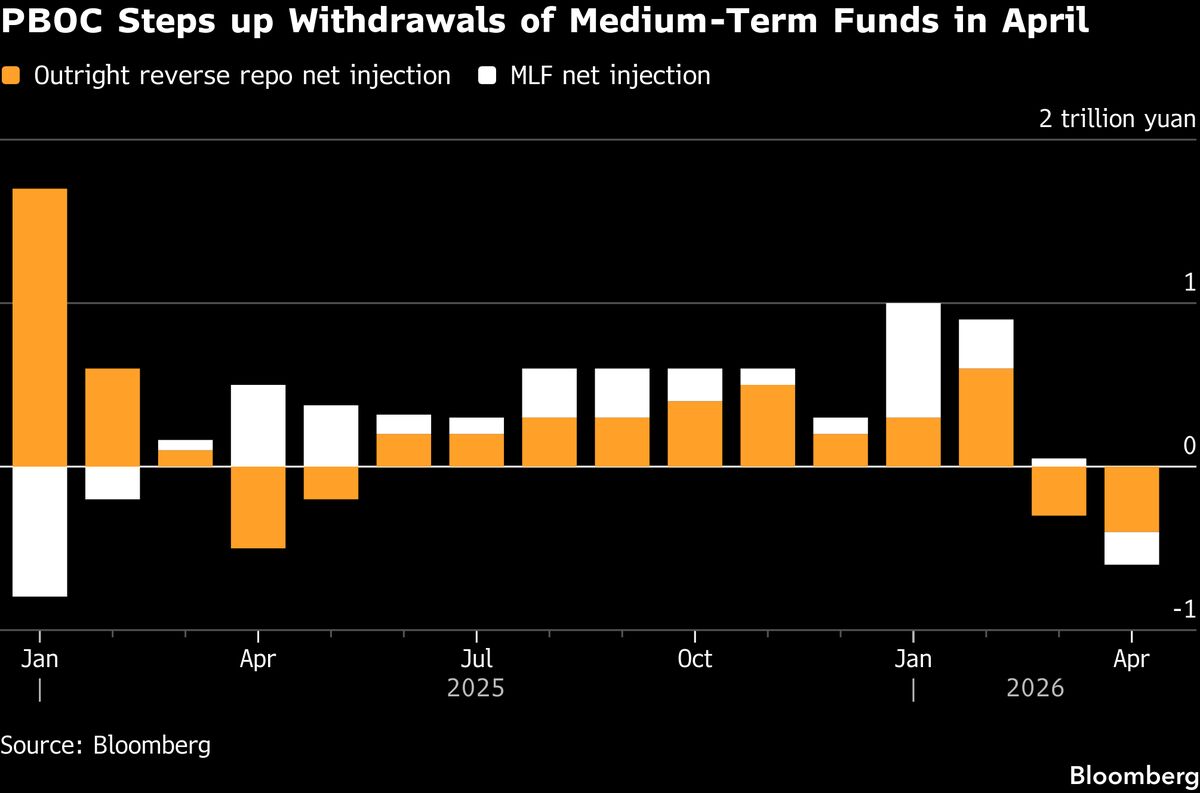

The People’s Bank of China (PBOC) announced it would reduce the volume of its medium-term lending facility (MLF) loans—a key tool for managing liquidity—marking the latest step in a gradual shift away from pandemic-era stimulus measures. While the cut was modest, analysts say it reflects Beijing’s growing focus on preventing speculative bubbles and stabilizing the yuan amid global market volatility.

A Strategic Pullback from Pandemic Stimulus

The PBOC’s decision comes as China’s economy shows tentative signs of recovery, with recent data indicating a rebound in factory activity and consumer spending. However, structural challenges persist, including a property sector downturn, weak export demand, and mounting local government debt.

Unlike Western central banks, which have aggressively raised interest rates to combat inflation, China has maintained a relatively loose monetary stance since 2020 to cushion the economic impact of COVID-19. But with liquidity levels now exceeding pre-pandemic norms, policymakers appear keen to avoid overstimulation that could fuel asset price inflation or capital outflows.

“The PBOC is walking a fine line,” said Li Wei, an economist at Shanghai’s Fudan University. “Too much tightening could stifle growth, but excessive liquidity risks distorting credit allocation and weakening the currency.”

How the MLF Works—And Why It Matters

The MLF program, introduced in 2014, allows the PBOC to inject funds into the banking system with maturities ranging from three months to a year. By adjusting MLF volumes and interest rates, the central bank indirectly influences broader lending conditions, including the benchmark loan prime rate (LPR), which affects corporate and household borrowing costs.

Today’s move follows a series of incremental adjustments, including smaller-than-expected cuts to reserve requirement ratios (RRR) for banks earlier this year. Market watchers interpret these steps as part of a broader strategy to guide credit toward productive sectors—such as advanced manufacturing and green energy—while deflating speculative investments in real estate and shadow banking.

Global Implications and Market Reactions

The PBOC’s cautious tightening contrasts sharply with the U.S. Federal Reserve’s hawkish stance, creating a divergence that has pressured the yuan and complicated China’s efforts to stabilize cross-border capital flows. The currency has lost nearly 4% against the dollar this year, prompting sporadic interventions by state-owned banks to smooth volatility.

Asian markets reacted cautiously to the news, with the Shanghai Composite Index dipping 0.3% in afternoon trading. Bond yields edged higher, reflecting expectations of tighter credit conditions.

“Investors are parsing whether this signals the start of a broader deleveraging campaign,” noted HSBC strategist Jason Liu. “For now, the PBOC seems to favor targeted adjustments over blunt force measures.”

Balancing Growth and Stability

China’s leadership has repeatedly emphasized “high-quality growth” over rapid expansion, a priority underscored by Premier Li Qiang’s recent calls for “precision” monetary policy. The approach mirrors longer-term goals to reduce reliance on debt-driven infrastructure spending and property speculation—a shift that has already contributed to defaults among overleveraged developers like Evergrande and Country Garden.

Still, analysts warn that excessive tightening could exacerbate deflationary pressures. Consumer prices rose just 0.1% year-on-year in September, while factory-gate prices contracted for the 12th consecutive month, underscoring weak domestic demand.

What Comes Next?

Most economists expect the PBOC to maintain a neutral-to-cautious stance in the coming months, with further RRR cuts possible if growth falters. However, large-scale stimulus akin to the 2008 financial crisis or 2020 pandemic response appears unlikely.

“The era of cheap money is ending, but not abruptly,” said ING’s Greater China head Iris Pang. “China’s policymakers are threading the needle—supporting key industries without reigniting financial risks.”

As global central banks grapple with inflation and recession fears, China’s measured approach offers a case study in calibrated monetary restraint. The challenge lies in sustaining momentum without repeating past excesses. For now, the PBOC’s latest move suggests stability remains the ultimate benchmark.

—Reporting by [Your Name]; additional analysis from financial markets and policy experts.