Dollar Dominance Expected to Continue as BMO Strategist Backs Long USD Position

By [Your Name], Senior Financial Correspondent

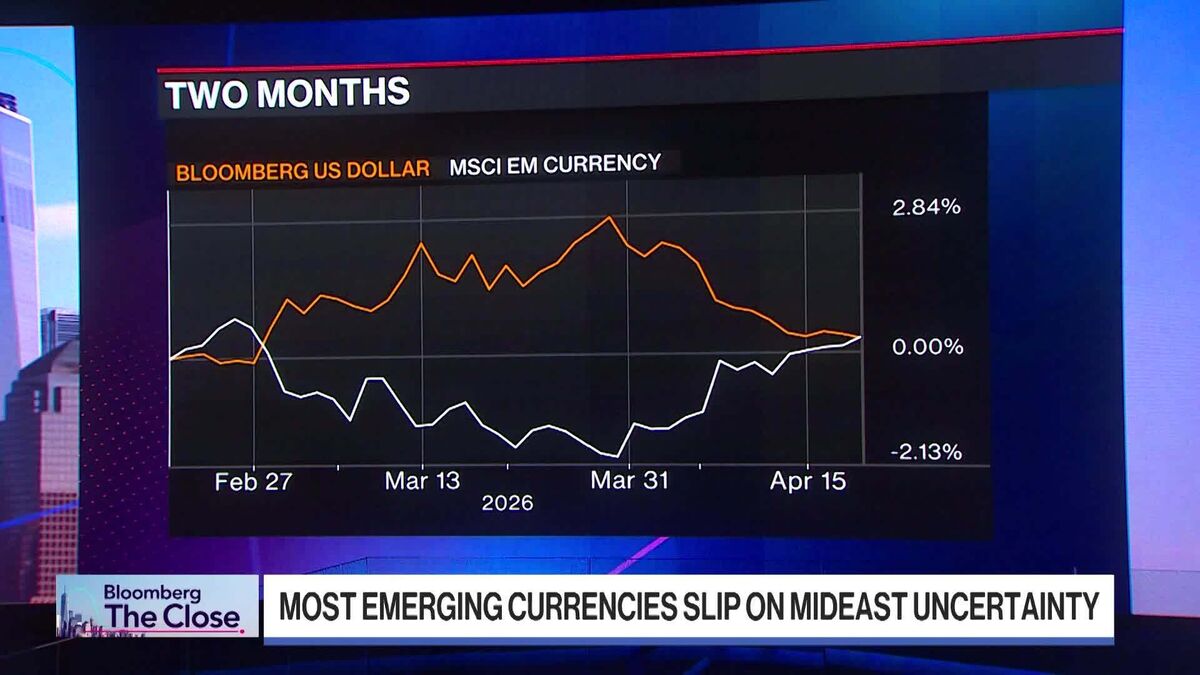

Global Currency Markets Brace for Extended Dollar Strength

The US dollar is poised to maintain its supremacy in global currency markets, with analysts predicting further gains as economic uncertainty and shifting monetary policies bolster its appeal. Mark McCormick, Global Head of FX Strategy at BMO Capital Markets, has reinforced this outlook, advocating for a long-dollar position in the near term. His comments, made during an interview on Bloomberg The Close, underscore a growing consensus among strategists that the greenback remains the safest harbor amid geopolitical tensions, stubborn inflation, and divergent central bank policies.

The dollar’s resilience has defied earlier expectations of a 2024 retreat, as robust US economic data and a cautious Federal Reserve continue to attract capital flows. McCormick’s analysis aligns with a broader market sentiment that sees the USD outperforming its peers—particularly the euro, yen, and pound—in the coming months.

Why the Dollar Still Reigns Supreme

The US dollar index (DXY), which measures the currency against a basket of six major counterparts, has surged nearly 5% year-to-date, reflecting sustained demand. Several factors underpin this trend:

-

Fed Policy Divergence – While the European Central Bank (ECB) and Bank of England (BoE) signal potential rate cuts later this year, the Fed has adopted a more patient stance. Strong labor markets and sticky inflation have forced policymakers to delay easing, keeping Treasury yields elevated and the dollar attractive for yield-seeking investors.

-

Safe-Haven Demand – Escalating conflicts in the Middle East, coupled with economic fragility in Europe and China, have driven capital into dollar-denominated assets. The currency’s status as the world’s primary reserve asset further solidifies its haven appeal.

-

Relative Economic Strength – The US economy continues to outpace its G10 counterparts, with Q1 GDP growth exceeding expectations. In contrast, the eurozone struggles with near-recessionary conditions, while Japan’s yen has plummeted to multi-decade lows amid a dovish Bank of Japan.

McCormick’s Case for a Long USD Trade

McCormick’s recommendation hinges on the interplay of these macroeconomic forces. “The dollar’s momentum isn’t fading anytime soon,” he noted, emphasizing that markets are still underpricing the Fed’s higher-for-longer narrative. He pointed to the widening interest rate differentials between the US and other developed economies as a key driver of dollar strength.

However, he cautioned that the trade is not without risks. A sudden dovish pivot by the Fed—triggered by an unexpected economic slowdown—could reverse gains. Additionally, intervention by Japanese authorities to prop up the yen or a resurgence in European growth might temper the dollar’s ascent.

Global Implications of a Strong Dollar

While dollar strength benefits US importers and travelers, it poses challenges for emerging markets and corporations with dollar-denominated debt. Countries like Turkey and Egypt face mounting pressure on their currencies, raising fears of capital flight. Meanwhile, multinational firms—particularly those in Europe and Asia—are grappling with reduced competitiveness as their exports become more expensive.

The euro, trading near five-month lows, reflects these strains. ECB officials have acknowledged the currency’s weakness but stopped short of direct intervention. Similarly, the yen’s slide past 160 against the dollar has sparked speculation that Tokyo may step in to stabilize the market.

Historical Context: A Cyclical Phenomenon

The dollar’s current rally echoes past cycles where Fed tightening and global instability fueled extended periods of USD appreciation. The 2014-2015 “taper tantrum” and the 2022 surge—driven by aggressive Fed hikes—serve as reminders of the currency’s enduring dominance.

Yet, history also suggests that dollar peaks are often followed by reversals. Analysts at Goldman Sachs and JPMorgan have warned that a US recession or a synchronized global recovery could erode the dollar’s edge later in 2024.

What Lies Ahead?

For now, traders are heeding McCormick’s advice, with CFTC data showing net long positions on the dollar at their highest since late 2022. The currency’s path will likely hinge on upcoming US inflation data and Fed commentary. A hotter-than-expected CPI print could reinforce bullish bets, while softer figures might trigger profit-taking.

As markets navigate this uncertain terrain, McCormick’s outlook serves as a timely reminder: in a world of uneven growth and policy divergence, the dollar remains the ultimate barometer of global risk sentiment. Whether its strength persists—or finally meets resistance—will depend on the delicate balance between US resilience and the rest of the world’s recovery.

For investors, the message is clear: bet against the dollar at your own peril—at least for now.