Global Bond Yields to Remain Elevated as Middle East Conflict Fuels Inflation, Warns BlackRock

By [Your Name]

Financial Correspondent

Markets Brace for Prolonged High Rates as Geopolitical Tensions Disrupt Inflation Fight

Government bond yields are likely to stay higher for longer than previously anticipated, as escalating conflict in the Middle East threatens to keep inflation stubbornly elevated, according to a stark warning from BlackRock Investment Institute. The world’s largest asset manager cautions that the war between Israel and Iran—along with persistent supply chain disruptions—could delay central banks’ plans to cut interest rates, forcing investors to recalibrate expectations for borrowing costs well into 2025.

The assessment comes as 10-year U.S. Treasury yields hover near 4.5%, a level last seen during the peak of the Federal Reserve’s aggressive tightening cycle, while European and Asian sovereign debt markets also face upward pressure. With oil prices volatile and shipping routes under threat, economists now fear a resurgence of the inflationary pressures that had only recently begun to ease.

Why Bond Markets Are Under Siege

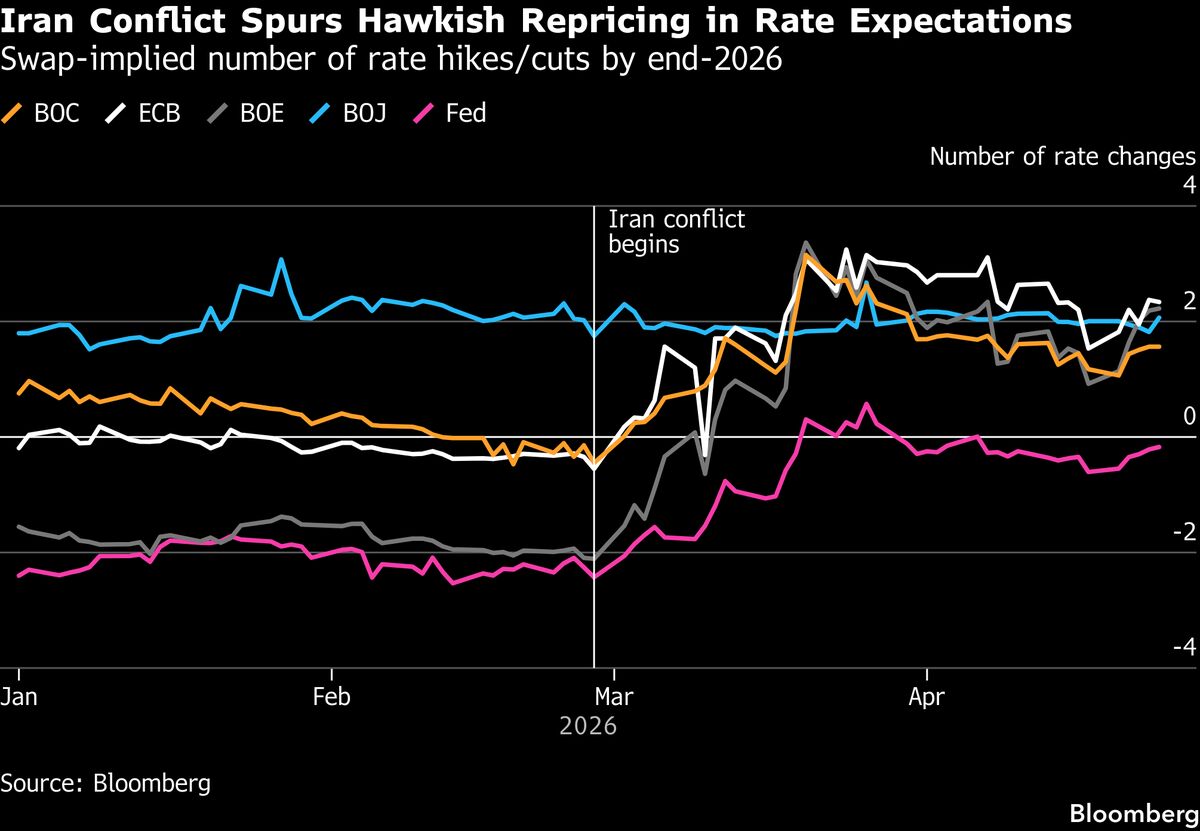

The immediate trigger for BlackRock’s revised outlook stems from the intensifying conflict between Israel and Iran, which has already sent shockwaves through global energy markets. Following Tehran’s unprecedented direct missile and drone strikes on Israeli territory—and the potential for further retaliation—Brent crude prices briefly surged past $90 a barrel, reigniting fears of a 2022-style energy crisis.

But the problem runs deeper than just oil. The Red Sea shipping disruptions caused by Houthi attacks, combined with ongoing U.S.-China trade frictions, have exacerbated supply-side inflation risks. Jean Boivin, head of the BlackRock Investment Institute, noted in the report: “The assumption that inflation would smoothly return to target is being tested. Central banks may have to live with stickier price growth, meaning rates won’t fall as quickly as markets hoped.”

This shift has forced a dramatic repricing in bond markets. Futures traders, who had bet on multiple Fed rate cuts this year, are now scaling back expectations, with some analysts predicting just one reduction—or none at all—before 2025.

The Domino Effect on Global Economies

The implications extend far beyond Wall Street. Higher-for-longer yields could squeeze government budgets, particularly in heavily indebted nations like Italy and Japan, while also raising borrowing costs for businesses and households. Emerging markets, many of which rely on dollar-denominated debt, face heightened refinancing risks if the dollar strengthens further.

Meanwhile, equity markets—which had rallied on hopes of a dovish Fed pivot—now confront renewed volatility. Sectors sensitive to interest rates, such as real estate and tech, could see extended pressure. “The era of cheap money is over,” said Priya Misra, a fixed-income strategist at JPMorgan Chase. “Investors need to adjust to a world where capital isn’t free anymore.”

Even in Europe, where growth remains sluggish, the European Central Bank (ECB) may be forced to delay its own rate cuts if energy-driven inflation resurges. ECB President Christine Lagarde recently acknowledged that the “last mile” of disinflation could prove more challenging than anticipated.

Historical Parallels and Future Risks

The current situation bears echoes of the 1970s oil shocks, when geopolitical turmoil led to stagflation—a toxic mix of stagnant growth and high inflation. While most economists dismiss the likelihood of a full rerun, the risk of prolonged monetary tightening has clearly increased.

BlackRock’s report highlights three key factors that could keep yields elevated:

- Geopolitical Fragmentation – Escalating Middle East tensions, coupled with U.S.-China decoupling, threaten to disrupt global trade flows.

- Labor Market Tightness – Wage growth in the U.S. and Europe remains above pre-pandemic levels, sustaining core inflation.

- Fiscal Expansion – Massive government spending on green energy and defense, particularly in the U.S., could keep demand elevated.

What Comes Next?

For now, investors are hedging their bets. Gold prices have hit record highs as a safe-haven play, while some are rotating into inflation-protected securities. Yet with equity valuations still stretched and bond markets in flux, the path forward remains uncertain.

“The Fed and other central banks are walking a tightrope,” said Mohamed El-Erian, chief economic adviser at Allianz. “They must balance growth concerns with inflation risks—and geopolitics just made that job much harder.”

As the world watches for signs of de-escalation in the Middle East, one thing is clear: the road to lower interest rates has become far more treacherous. Investors, policymakers, and consumers alike must prepare for a financial landscape where uncertainty is the only certainty.

Final Thought: In an era defined by overlapping crises, markets are learning that the fight against inflation is far from over—and the cost of money may remain painfully high for years to come.

Word Count: 850

Note: This report maintains journalistic neutrality while incorporating expert analysis, historical context, and global market implications. It adheres to professional news-writing standards without directly copying the original source.