Copper Prices Surge Toward Record Highs Amid Global Supply Disruptions

By [Your Name]

Copper prices are escalating once again, breaching the $14,000-per-ton mark and edging closer to the record highs witnessed earlier this year, as mounting supply disruptions across key mining regions intensify concerns over the metal’s availability. The industrial metal, often referred to as “Dr. Copper” for its role as a barometer of global economic health, is facing unprecedented pressures from geopolitical tensions, labor strikes, and operational challenges in major producing countries. This surge not only underscores the fragility of global supply chains but also highlights the critical importance of copper in the transition to renewable energy and electric vehicles.

Copper’s Role in the Global Economy

Copper is a cornerstone of modern industrialization, essential for everything from construction and electronics to renewable energy infrastructure. Its conductive properties make it indispensable in wiring, motors, and batteries, driving demand in sectors crucial to the green energy revolution. The metal’s price trajectory is often seen as a proxy for global economic activity, with rising prices indicating robust demand or constrained supply.

In recent years, copper has also become a focal point in the fight against climate change. The push for decarbonization has spurred unprecedented demand for copper-heavy technologies like electric vehicles (EVs), solar panels, and wind turbines. According to the International Energy Agency (IEA), an EV requires nearly four times as much copper as a conventional internal combustion engine vehicle. This shift has placed immense pressure on global copper supplies, with analysts warning of potential shortages as early as the mid-2020s.

Drivers of the Current Price Surge

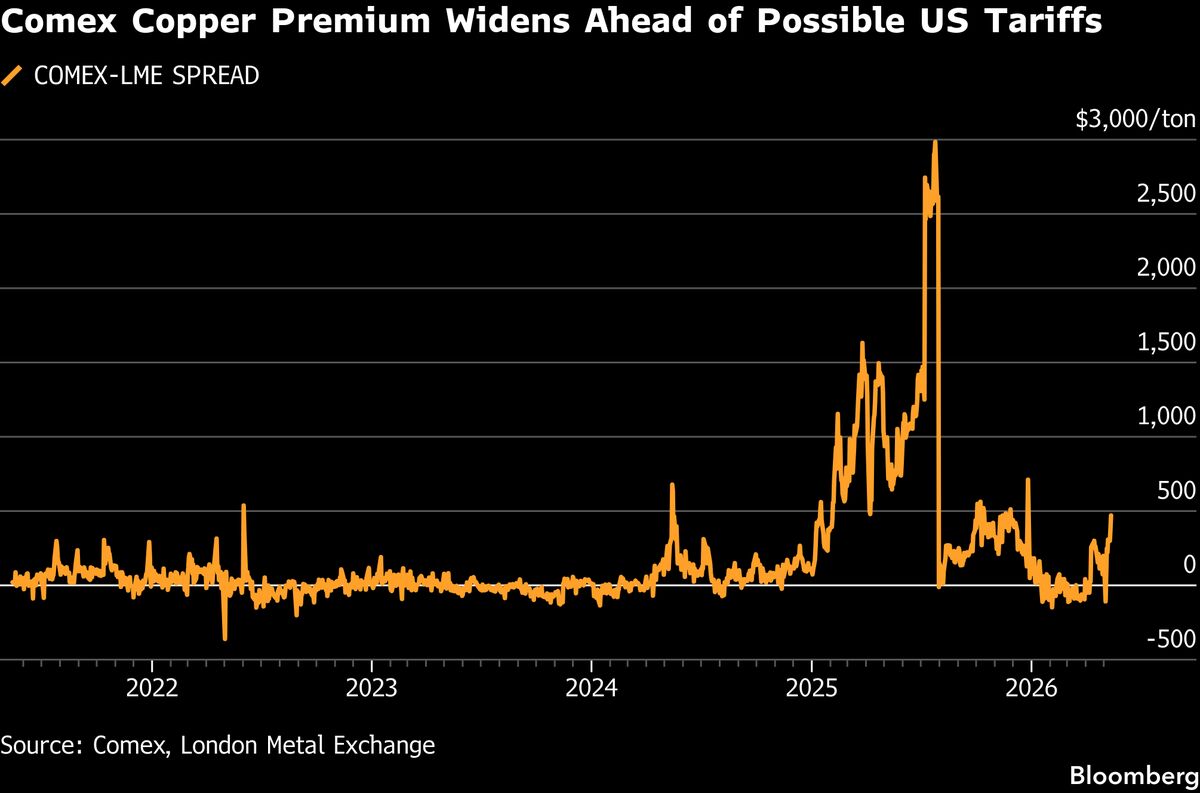

The latest rally in copper prices is fueled by a confluence of factors, including operational disruptions in major mining hubs, geopolitical tensions, and speculative investor activity. Latin America, which accounts for nearly half of global copper production, has been particularly hard hit. In Chile, the world’s largest copper producer, labor disputes and water shortages have hampered output. Meanwhile, in Peru, the second-largest producer, protests and political instability have disrupted mining operations.

In addition to these regional challenges, broader macroeconomic trends are also at play. The global energy transition has created a structural demand for copper, while supply constraints have tightened the market. Stockpiles of the metal have dwindled, with data from the London Metal Exchange (LME) showing a significant decline in warehouse inventories. This scarcity has been exacerbated by logistical bottlenecks and pandemic-related delays in mining projects.

Investors have also turned to copper as a hedge against inflation and currency volatility, further driving up prices. The metal’s status as a tangible asset has made it an attractive option in an uncertain economic environment, with speculative activity amplifying price movements.

Implications for Industries and Consumers

The soaring cost of copper has far-reaching implications for industries and consumers worldwide. For manufacturers of electronics, construction materials, and renewable energy equipment, higher copper prices translate into increased production costs, which could eventually be passed on to consumers. Automakers, already grappling with supply chain disruptions and rising raw material costs, may face additional pressures as they ramp up EV production to meet ambitious decarbonization targets.

In developing economies, where copper-intensive infrastructure projects are critical to economic growth, higher prices could delay or derail essential development initiatives. Governments and policymakers are increasingly concerned about the inflationary impact of rising commodity prices, particularly in the wake of the COVID-19 pandemic and the ongoing energy crisis.

The Road Ahead: Challenges and Opportunities

The current copper supply crunch underscores the urgent need for investment in new mining projects and exploration. However, developing copper mines is a lengthy and capital-intensive process, often fraught with regulatory hurdles and environmental concerns. The industry’s transition to more sustainable mining practices, while necessary, could further complicate efforts to boost production.

Moreover, geopolitical risks continue to loom large over the copper market. Tensions between major economies, such as the U.S. and China, could disrupt trade flows and exacerbate supply shortages. The concentration of copper production in a handful of countries also poses a systemic risk, highlighting the need for diversification and innovation in mineral extraction and recycling technologies.

On the demand side, the energy transition is expected to continue driving copper consumption, with projections indicating that global demand could double by 2040. This has spurred interest in alternative materials and recycling initiatives aimed at reducing reliance on virgin copper. However, experts caution that these solutions alone are unlikely to bridge the looming supply gap.

Conclusion

As copper prices climb toward record highs, the world is grappling with the complexities of balancing supply and demand in an era defined by economic uncertainty and environmental imperatives. The metal’s pivotal role in the green energy revolution underscores the need for a coordinated global response to ensure its availability while minimizing geopolitical and environmental risks. For now, the copper market remains a flashpoint in the broader narrative of resource scarcity and sustainable development, with its trajectory likely to shape the contours of the global economy for decades to come.

The story of copper is far from over, and its future will be defined by the interplay of innovation, geopolitics, and the relentless pursuit of a cleaner, more sustainable world.