Wall Street Banks Tighten Credit Lines to Private Equity, Squeezing $1.2 Trillion Industry

By [Your Name], Financial Correspondent

New York/London — A seismic shift is underway in the world of private credit as Wall Street banks, once enthusiastic enablers of the $1.2 trillion industry, begin pulling back on the leverage that fueled its meteoric rise. Major financial institutions are now tightening lending terms to private credit funds, compounding challenges for an industry already grappling with investor withdrawals, rising defaults, and a high-interest-rate environment. The move marks a stark reversal from years of aggressive expansion, raising questions about the sustainability of private credit’s breakneck growth and its broader implications for global financial markets.

The Leverage Lifeline Dries Up

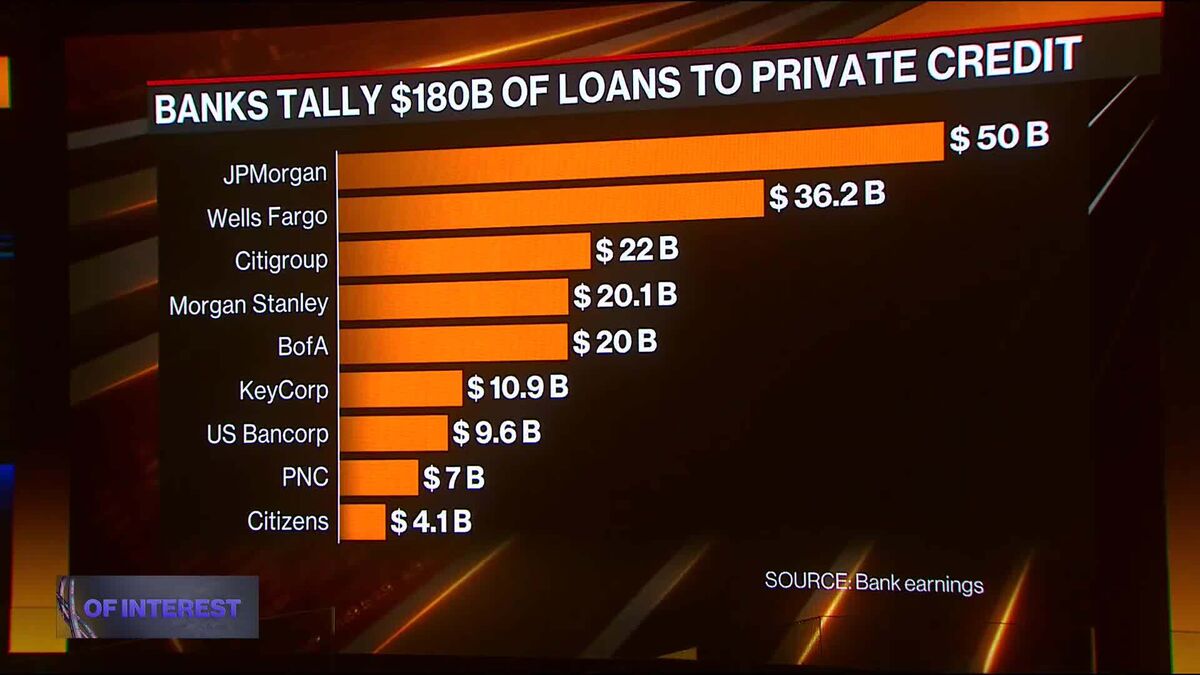

For over a decade, private credit funds—which provide loans to corporations outside traditional banking channels—relied heavily on leverage provided by investment banks to supercharge their returns. These so-called “subscription lines” allowed funds to borrow against investor commitments, effectively magnifying their purchasing power and enabling larger deals. According to data from Preqin, the private credit market ballooned from $500 billion in 2015 to over $1.2 trillion today, with Wall Street banks like Goldman Sachs, JPMorgan Chase, and Citigroup acting as key financiers.

Now, those same banks are scaling back. Sources familiar with the matter say lenders are shortening loan maturities, increasing collateral requirements, and in some cases, refusing to roll over credit lines altogether. The tightening comes as regulators scrutinize banks’ exposure to private funds and defaults in the sector creep upward.

“Banks are reassessing risk across the board, and private credit is no exception,” said Claudia Mitchell, a senior analyst at Bernstein Research. “The days of easy leverage are over, at least for now.”

A Perfect Storm for Private Credit

The withdrawal of bank financing exacerbates existing pressures in the private credit market. Rising interest rates have made borrowing more expensive, while economic uncertainty has led institutional investors—including pensions and endowments—to pull capital from private funds in favor of safer assets. Redemption requests hit a five-year high in 2023, according to data from McKinsey & Co., leaving fund managers scrambling for liquidity.

Compounding the pain, corporate defaults in private credit portfolios have risen sharply. S&P Global reported a default rate of 3.2% among privately placed loans in 2023, up from 1.8% the previous year. Sectors like commercial real estate, retail, and healthcare—where private credit has been heavily deployed—are particularly vulnerable.

“The triple whammy of higher rates, investor redemptions, and now tighter bank credit is forcing managers to rethink their strategies,” said Daniel Rothman, a partner at law firm Simpson Thacher. “Some may have to sell assets at a discount or turn away new deals altogether.”

Regulatory Pressure and the Shadow Banking Debate

The retreat of Wall Street banks also reflects growing regulatory unease over the risks posed by private credit. U.S. and European authorities have warned that the sector’s opacity and rapid growth could create systemic vulnerabilities, particularly if leveraged loans sour en masse. The Federal Reserve has privately urged banks to reduce exposure to private funds, according to people familiar with the discussions.

Critics argue that private credit operates in a regulatory gray zone, escaping the stringent capital requirements imposed on traditional lenders. “This is shadow banking at its most opaque,” said Sheila Warren, CEO of the Crypto Council for Innovation and a former World Bank official. “If defaults spike, we could see contagion effects rippling through the broader financial system.”

Proponents, however, insist that private credit plays a vital role in financing mid-market companies underserved by conventional banks. “Private credit fills a critical gap, especially for firms that don’t qualify for syndicated loans,” said Michael Arougheti, CEO of Ares Management, one of the largest private credit managers. “The market is maturing, not collapsing.”

What Comes Next?

The immediate fallout is likely to include consolidation, as smaller funds struggle to secure financing while larger players with stronger balance sheets absorb their assets. Some analysts predict a wave of distressed sales in the coming months, particularly in sectors like office real estate and leveraged buyouts.

Longer-term, the industry may pivot toward more conservative structures, such as longer-duration funds with lower leverage ratios. “This is a wake-up call,” said Rothman. “Funds that relied on cheap debt to juice returns will need to adapt or face extinction.”

As Wall Street’s love affair with private credit cools, the broader question remains: Is this a temporary correction or the beginning of a more profound reckoning for one of finance’s fastest-growing sectors? For now, the only certainty is that the era of easy money is over.