Fukoku Mutual Scales Back Japanese Government Bond Purchases Amid Yield Concerns

By [Your Name], Senior Financial Correspondent

Tokyo, Japan – In a strategic shift reflecting broader market anxieties, Japan’s Fukoku Mutual Life Insurance Co. has announced plans to significantly reduce its purchases of Japanese government bonds (JGBs) this fiscal year, citing diminishing returns in the super-long-term debt segment. The move underscores growing institutional skepticism toward Japan’s ultra-low-yield environment, even as the Bank of Japan (BOJ) maintains its controversial monetary easing policies.

With over ¥7.5 trillion ($48 billion) in assets under management, Fukoku’s decision carries weight in a market where life insurers are traditionally among the largest holders of sovereign debt. The firm’s pivot signals a broader reassessment of risk among institutional investors, who are increasingly questioning the sustainability of Japan’s debt-driven fiscal strategy amid global inflationary pressures and a weakening yen.

A Retreat from Tradition

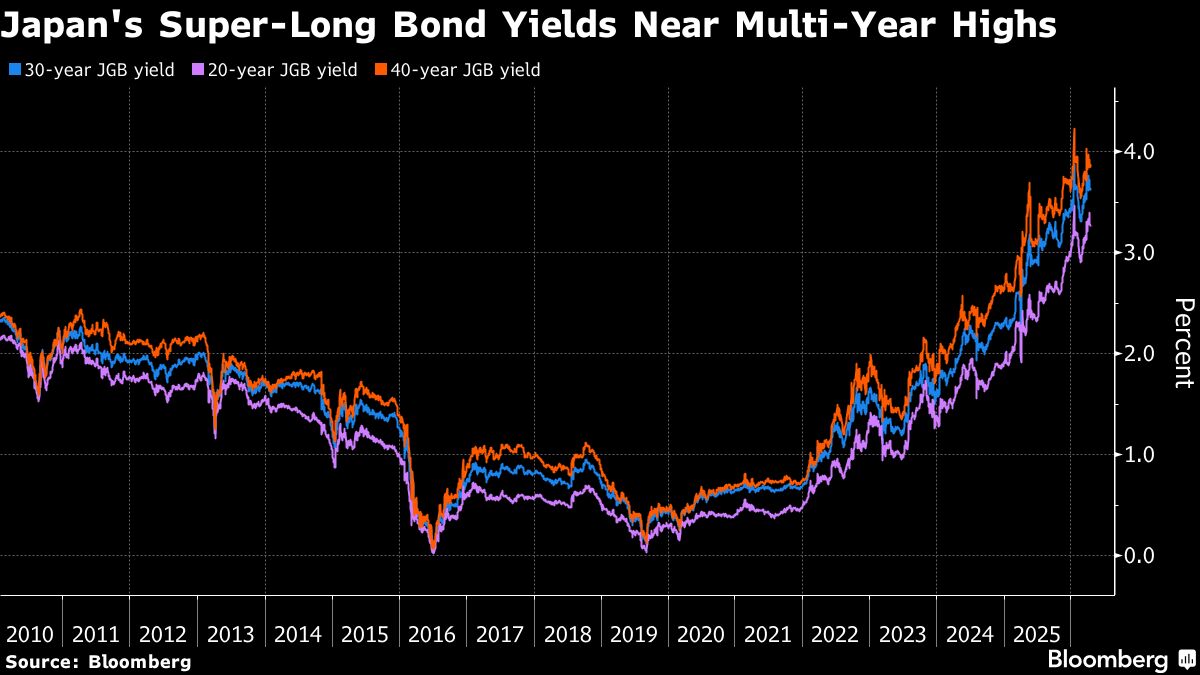

For decades, Japanese life insurers like Fukoku have been stalwart buyers of JGBs, drawn by their perceived safety and alignment with long-term liabilities. However, with 30-year yields hovering near 1.7%—far below inflation-adjusted returns in other major economies—the calculus is changing. “The upside for super-long yields is limited, and we see better opportunities elsewhere,” a Fukoku executive told reporters, hinting at allocations to foreign bonds and alternative assets.

The insurer’s pullback comes as Japan grapples with a paradox: despite the BOJ’s negative interest rate policy and yield curve control (YCC), demand for long-dated JGBs has waned. In April, a poorly received 30-year bond auction saw tepid bidding, a red flag for policymakers. Analysts warn that Fukoku’s stance could embolden other institutional investors to follow suit, further straining Japan’s ability to finance its towering public debt, which exceeds 260% of GDP.

Global Context: The BOJ’s Dilemma

Japan’s bond market woes mirror a global trend of investors fleeing low-yielding sovereign debt as central banks elsewhere maintain higher rates. The U.S. 10-year Treasury, for instance, offers around 4.3%, while Germany’s Bunds yield roughly 2.5%—both far eclipsing JGBs. This disparity has accelerated capital outflows, exacerbating the yen’s decline to 34-year lows against the dollar.

The BOJ faces mounting pressure to normalize policy after its landmark March rate hike—the first in 17 years—failed to revive bond appeal. Governor Kazuo Ueda has cautiously signaled further tightening, but analysts doubt aggressive moves are imminent. “The BOJ is trapped,” said Naomi Fink, a strategist at Nikko Asset Management. “Higher rates could destabilize Japan’s debt servicing, but inaction risks deeper investor disillusionment.”

Domestic Ripples and Fiscal Risks

Fukoku’s retreat also highlights vulnerabilities in Japan’s financial ecosystem. Banks and pension funds, already squeezed by narrow margins, may face heavier burdens as insurers retreat from bond auctions. Meanwhile, the government’s reliance on domestic buyers—who hold about 90% of JGBs—could be tested if defections multiply.

Prime Minister Fumio Kishida’s administration has downplayed concerns, emphasizing Japan’s “stable” debt ownership structure. Yet economists note that demographic decline—a shrinking pool of domestic savers—threatens this model. “The era of endless JGB demand is ending,” said Jesper Koll, an adviser to WisdomTree Investments. “Japan must either attract foreign buyers or risk fiscal turbulence.”

Alternatives and the Search for Yield

Fukoku’s shift mirrors a broader industry trend. Dai-ichi Life and Nippon Life have similarly trimmed JGB holdings in favor of U.S. corporate bonds and infrastructure debt. Foreign assets now account for over 25% of Japanese insurers’ portfolios, a record high.

Yet currency risk looms large. The yen’s depreciation has inflated hedging costs, eroding returns. Some insurers are absorbing the hit, betting on eventual BOJ intervention. Others are diversifying into private equity and renewables—a risky gambit for traditionally conservative institutions.

What’s Next?

Market watchers will scrutinize the BOJ’s June meeting for clues on YCC adjustments. Any hint of tapering bond purchases could trigger volatility, given Japan’s outsized role in global debt markets. For Fukoku, the path forward is clear: “We must adapt to survive,” its CFO recently remarked.

As Japan’s economic experiment enters uncharted territory, the world is left to ponder a delicate question: Can the BOJ balance stability with the need to lure back skeptical investors? The answer may reshape not just Japan’s financial landscape, but the global bond market itself.

Reporting contributed by [Your Name] in Tokyo and [Colleague’s Name] in London. Additional data from Bloomberg and the Ministry of Finance Japan.