Global Markets Brace for Volatility as Analysts Warn of June Profit-Taking

By [Your Name], Financial Correspondent

June 3, 2024 — Global equities face a pivotal moment as investors weigh the risks of overexuberance against stubborn inflationary pressures, setting the stage for potential turbulence in the weeks ahead. Bank of America strategists have issued a stark warning that crowded trades and stretched valuations could trigger a wave of profit-taking this month, testing the resilience of a market that has largely shrugged off macroeconomic headwinds in 2024.

A Market at a Crossroads

The S&P 500’s 11% year-to-date rally—driven by AI optimism and resilient corporate earnings—now confronts mounting skepticism as central banks delay rate cuts amid sticky inflation. BofA’s research team notes that investor positioning has reached “overbought” territory, with hedge funds and retail traders alike piling into tech and growth stocks. This herd mentality, coupled with fading hopes for near-term monetary easing, creates what analysts describe as a “powder keg” scenario where even minor shocks could spark a pullback.

“The market is pricing in perfection,” said Michael Hartnett, BofA’s chief investment strategist, in a client note. “When everyone leans the same way, liquidity evaporates fastest.” Historical data supports this caution: June has historically been the weakest month for the S&P 500, averaging a 0.7% decline over the past 20 years.

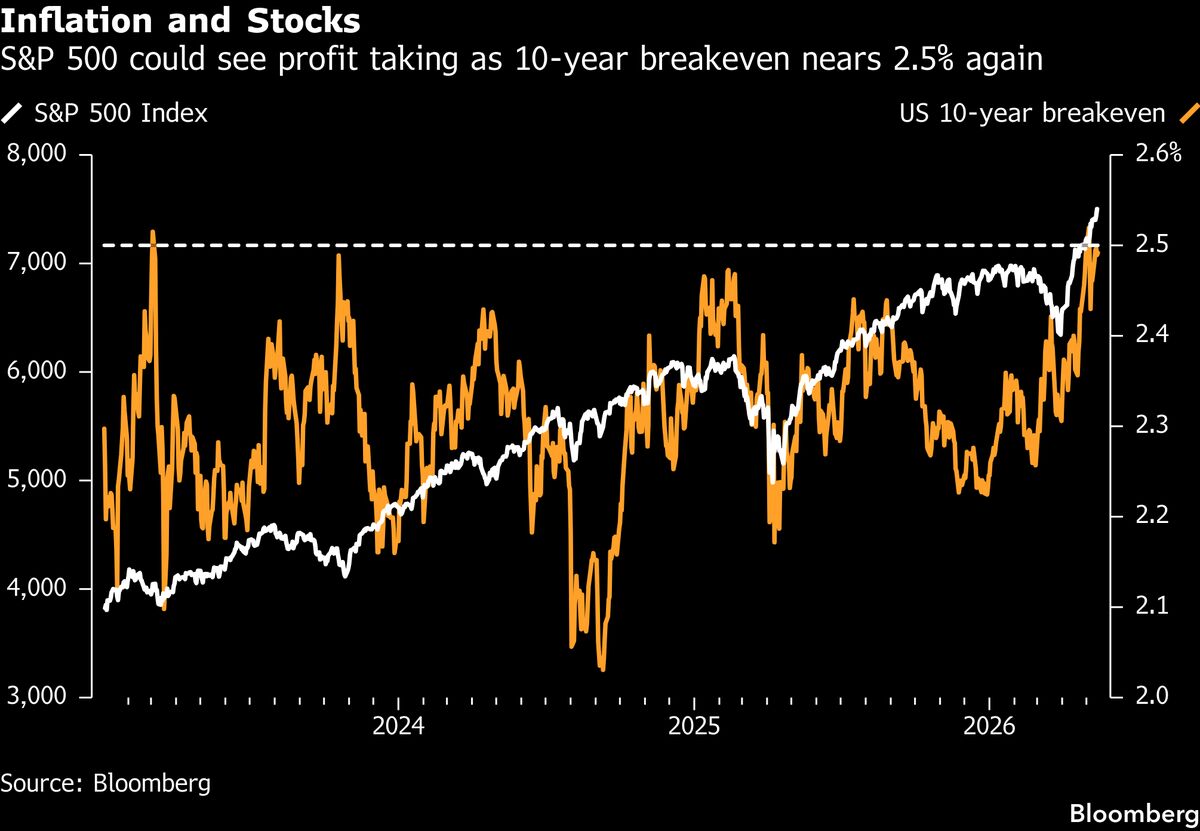

Inflation: The Uninvited Guest

While equities have climbed a wall of worry in 2024—from Middle East tensions to lackluster Chinese demand—inflation remains the thorniest challenge. The latest U.S. core PCE data, the Federal Reserve’s preferred gauge, showed prices rising at an annualized 2.8% in April, well above the central bank’s 2% target. Similar trends in the eurozone and emerging markets have forced policymakers to maintain restrictive rates, squeezing the cheap-money lifeline that fueled past rallies.

“The ‘higher for longer’ narrative is back with a vengeance,” noted Claudia Sahm, a former Fed economist. “Investors betting on a summer rate cut are likely to be disappointed.” Bond markets reflect this shift, with 10-year Treasury yields creeping back toward 4.5%, pressuring equity valuations.

Sector Vulnerabilities and Safe Havens

Tech stocks—particularly the “Magnificent Seven” megacaps—are seen as most exposed to a correction after their 30% collective surge this year. However, cyclical sectors like industrials and small-caps could face even steeper declines if growth fears intensify.

In contrast, defensive plays are gaining traction:

- Gold has rallied 15% year-to-date as a hedge against currency debasement and geopolitical risks.

- Energy stocks are benefiting from elevated oil prices, with Brent crude holding above $80 despite OPEC+ supply hikes.

- Japanese yen assets have attracted flows as the Bank of Japan signals a gradual exit from ultra-loose policies.

Global Ripple Effects

The profit-taking warning isn’t confined to Wall Street. European bourses, already lagging U.S. peers due to sluggish growth, face added pressure from political uncertainty as EU parliamentary elections loom. Meanwhile, emerging markets grapple with dollar strength; India’s Sensex and Brazil’s Bovespa have underperformed amid foreign outflows.

China remains a wild card. Despite recent stimulus measures, its property crisis and weak consumer spending continue to drag on regional sentiment. “The world’s second-largest economy isn’t providing the counterbalance it once did,” said HSBC’s Asia equity strategist Herald van der Linde.

What Comes Next?

For now, the bull case hinges on corporate earnings sustaining their momentum. Q1 profits grew 5.5% year-over-year, but Q2 forecasts are less rosy, with analysts penciling in just 3.8% growth. Any misses could accelerate selling.

Yet not all strategists foresee doom. Goldman Sachs maintains its year-end S&P 500 target of 5,200 (versus today’s 5,100), arguing that AI-driven productivity gains will offset rate concerns. “The secular bull market isn’t over,” said David Kostin, the bank’s U.S. equity chief. “But the road will get bumpier.”

A Delicate Balance

As traders navigate June’s historical seasonality and shifting macro winds, the lesson is clear: markets rarely move in straight lines. Whether this month brings a healthy correction or a deeper rout depends on inflation’s next act—and whether investors remember that trees don’t grow to the sky.