India’s Central Bank Faces Uphill Battle to Stabilize the Rupee as Global Pressures Mount

By [Your Name], Financial Correspondent

MUMBAI, India—India’s central bank is bracing for another tough fight to defend the rupee as global financial turbulence and a resurgent U.S. dollar threaten to destabilize emerging markets. With the currency hovering near historic lows, policymakers at the Reserve Bank of India (RBI) may need to revisit strategies from past crises—including the 2013 “taper tantrum” and earlier balance-of-payments emergencies—to prevent a full-blown currency meltdown.

The rupee has been under relentless pressure in recent months, battered by a potent mix of rising U.S. interest rates, stubborn inflation, and widening trade deficits. Analysts warn that without decisive intervention, India risks repeating the painful currency crises that have rocked its economy in previous decades.

A Currency Under Siege

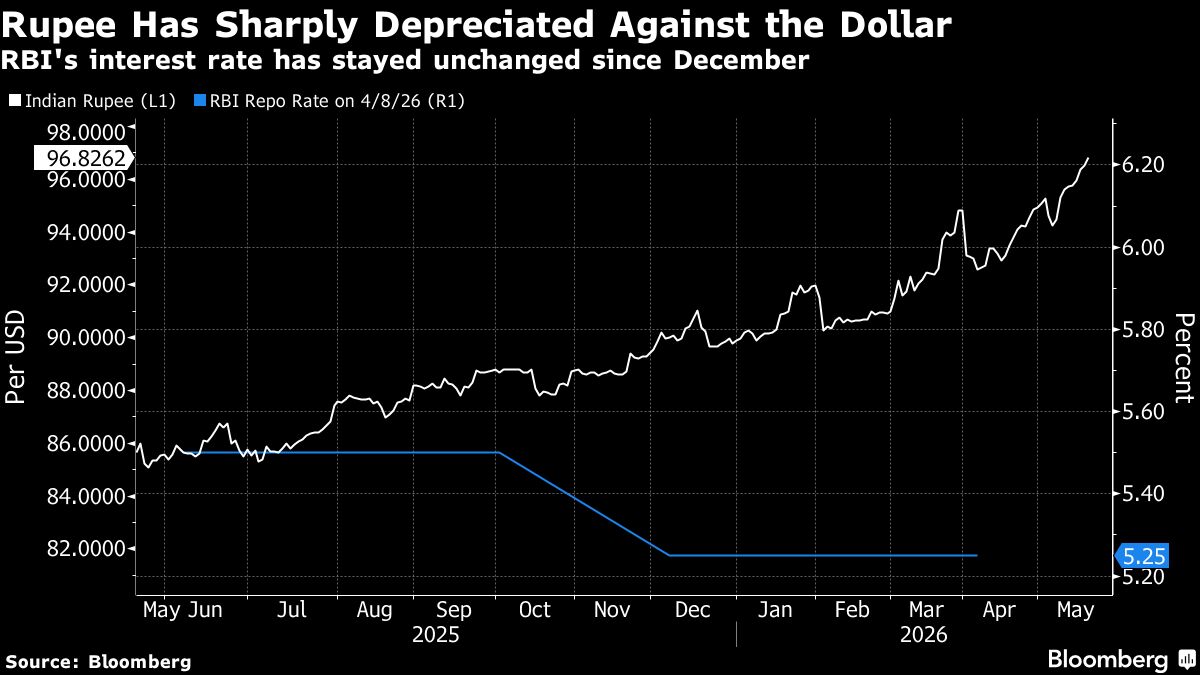

The Indian rupee has depreciated by nearly 10% against the U.S. dollar over the past year, breaching the psychologically critical 83-per-dollar mark multiple times. While some depreciation is expected given the Federal Reserve’s aggressive monetary tightening, the speed and scale of the rupee’s decline have raised alarms.

“The RBI is walking a tightrope,” said Priyanka Kishore, head of India and Southeast Asia economics at Oxford Economics. “They must balance defending the rupee without exhausting foreign reserves or triggering capital flight.”

India’s foreign exchange reserves, once a robust buffer at over $600 billion, have dwindled to around $580 billion as the RBI sells dollars to prop up the rupee. Yet unlike 2013—when the Fed’s taper announcement triggered a panic in emerging markets—today’s challenges are compounded by high oil prices, slowing global growth, and geopolitical tensions.

Lessons from Past Crises

The RBI’s playbook for currency defense is well-tested but not foolproof. During the 2013 taper tantrum, India deployed a mix of capital controls, interest rate hikes, and dollar sales to stabilize the rupee. The crisis also forced long-overdue economic reforms, including easing foreign investment rules and reducing fiscal deficits.

A decade later, India’s economy is far stronger—boasting deeper forex reserves, lower external debt, and a more stable current account. However, external shocks remain a major vulnerability. Rising crude oil prices, in particular, threaten to widen India’s trade deficit, which hit a record $31.5 billion in July.

“The RBI has the tools to manage volatility, but it can’t fight global trends indefinitely,” said Ananth Narayan, a senior banking analyst. “If the dollar rally continues, India may need additional measures beyond forex intervention.”

Policy Dilemmas Ahead

The RBI’s options are narrowing as global headwinds intensify. Raising interest rates could attract foreign capital but risk stifling India’s post-pandemic recovery. Tightening liquidity further could also hurt small businesses already struggling with high borrowing costs.

Meanwhile, alternative measures—such as encouraging foreign bond inflows or securing dollar swap lines with other central banks—offer only temporary relief. Some analysts suggest India may need to accept a weaker rupee to maintain export competitiveness, though this could fuel imported inflation.

“The biggest risk is a loss of investor confidence,” said Radhika Rao, senior economist at DBS Bank. “If markets sense the RBI is running out of ammunition, speculative attacks on the rupee could accelerate.”

The Global Context

India is not alone in its currency woes. From Japan to Europe, central banks are grappling with dollar strength as the Fed signals more rate hikes. Emerging markets like Indonesia and the Philippines have also intervened heavily to support their currencies.

Yet India’s large domestic economy and strong growth outlook provide some insulation. Unlike in 1991—when the country nearly defaulted and was forced to pledge gold reserves—today’s India has a more diversified export base and a thriving tech sector.

“The RBI has the experience and resources to navigate this storm,” said Shilan Shah, India economist at Capital Economics. “But the longer global uncertainty persists, the harder it becomes to avoid collateral damage.”

What Comes Next?

With no immediate end in sight to Fed tightening, the RBI will likely continue its multi-pronged defense: intervening in forex markets, tightening capital controls if needed, and possibly coordinating with other Asian central banks to prevent competitive devaluations.

For now, most economists believe India can avoid a full-blown crisis—but the road ahead remains fraught with risks. As global financial conditions tighten, the RBI’s ability to strike the right balance between stability and growth will be tested like never before.

In the high-stakes game of currency defense, India’s central bank still holds some strong cards—but whether they will be enough remains to be seen.