Swiss National Bank Holds Firm on Franc Cap as Negative Rates Debate Intensifies

ZURICH, June 12, 2024 — The Swiss National Bank (SNB) is expected to reaffirm its commitment to capping the franc’s appreciation this week, opting for currency intervention over the more extreme measure of negative interest rates. As global markets remain volatile amid geopolitical tensions and shifting monetary policies, Switzerland’s central bank faces mounting pressure to balance economic stability with the risks of prolonged currency manipulation.

A Delicate Balancing Act

Since introducing its currency cap in 2011, the SNB has maintained a firm stance against excessive franc strength, which threatens Switzerland’s export-driven economy. The policy, which pegs the franc at 1.20 against the euro, has shielded Swiss manufacturers and tourism but drawn criticism for distorting market forces. Now, with the European Central Bank (ECB) and U.S. Federal Reserve signaling divergent monetary paths, the SNB’s next move is under intense scrutiny.

Analysts widely anticipate that policymakers will keep the status quo, avoiding negative interest rates—a tool last deployed in 2015—despite mounting speculation. “The SNB prefers targeted interventions over blanket negative rates, which carry long-term risks for banks and savers,” said Claudia Aebersold, chief economist at Zürcher Kantonalbank. “But the question is how long they can sustain this approach if global pressures escalate.”

Why Negative Rates Remain a Last Resort

Negative interest rates, while effective in weakening a currency, come with significant side effects. They erode bank profitability, discourage savings, and can fuel asset bubbles—a concern in Switzerland’s already overheated housing market. The SNB’s previous foray into sub-zero territory in 2015 led to backlash from domestic lenders and pension funds, making policymakers wary of repeating the experiment.

Instead, the bank has relied on foreign exchange (FX) interventions, purchasing euros and dollars to suppress franc demand. Data from the Bank for International Settlements (BIS) shows the SNB spent over CHF 90 billion ($100 billion) in 2023 alone to stabilize the exchange rate. Yet, with inflation subdued and the Swiss economy growing modestly, critics argue that further interventions may be unnecessary—or even counterproductive.

Global Pressures and the Inflation Puzzle

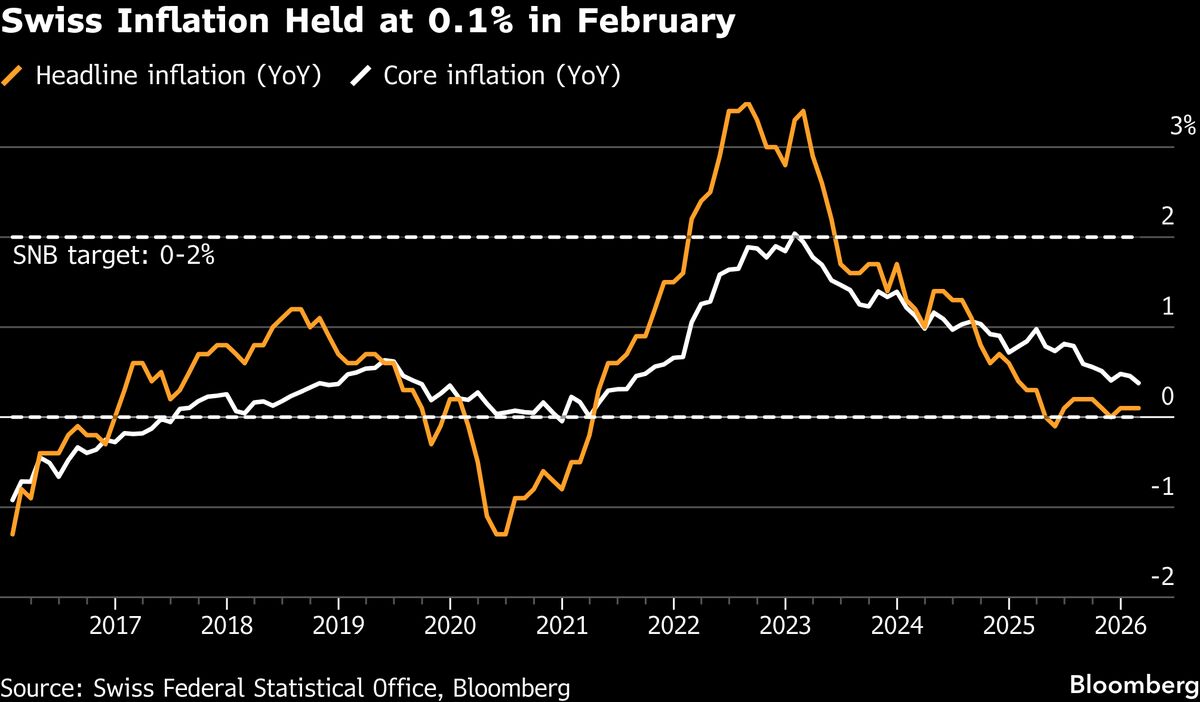

Switzerland’s inflation rate, currently at 1.4%, remains well below the SNB’s 2% target, reducing urgency for aggressive policy shifts. However, external factors loom large. The ECB’s potential rate cuts could widen the euro-franc divergence, while safe-haven demand—driven by Middle East tensions and U.S. election uncertainty—could trigger another franc surge.

“The SNB is walking a tightrope,” noted Markus Brunnermeier, an economist at Princeton University. “Too much intervention risks political backlash; too little could hurt exporters. Their challenge is to signal flexibility without committing to drastic steps prematurely.”

Market Reactions and Future Scenarios

Currency traders remain cautious ahead of the SNB’s announcement. While most expect no change in rates, any hint of future policy shifts—such as a readiness to impose negative rates if needed—could trigger market volatility. The franc has gained 3% against the euro this year, reflecting investor caution, but analysts say the SNB still has ample reserves to defend its cap if necessary.

Longer-term, however, Switzerland may need to reconsider its strategy. With the U.S. dollar strengthening and the ECB’s policy trajectory uncertain, the SNB’s toolkit could face new limits. Some economists suggest alternative measures, such as tiered deposit rates or targeted lending schemes, to ease pressure on the financial sector.

Conclusion: Stability Over Experimentation

For now, the SNB appears set to prioritize stability over radical moves. Its cautious approach reflects both the success of past interventions and the risks of untested policies in an unpredictable global economy. As one Zurich-based trader put it, “The SNB would rather fight the franc with reserves than with rates—because once you go negative, it’s hard to turn back.”

With global markets at a crossroads, Switzerland’s central bank is betting that steady hands will prove wiser than dramatic gestures. Whether that calculation holds may depend on forces far beyond its borders.