Debt Funds Double Market Share in UK Property Lending as Banks Retreat Amid Regulatory Pressure

By [Your Name], Senior Financial Correspondent

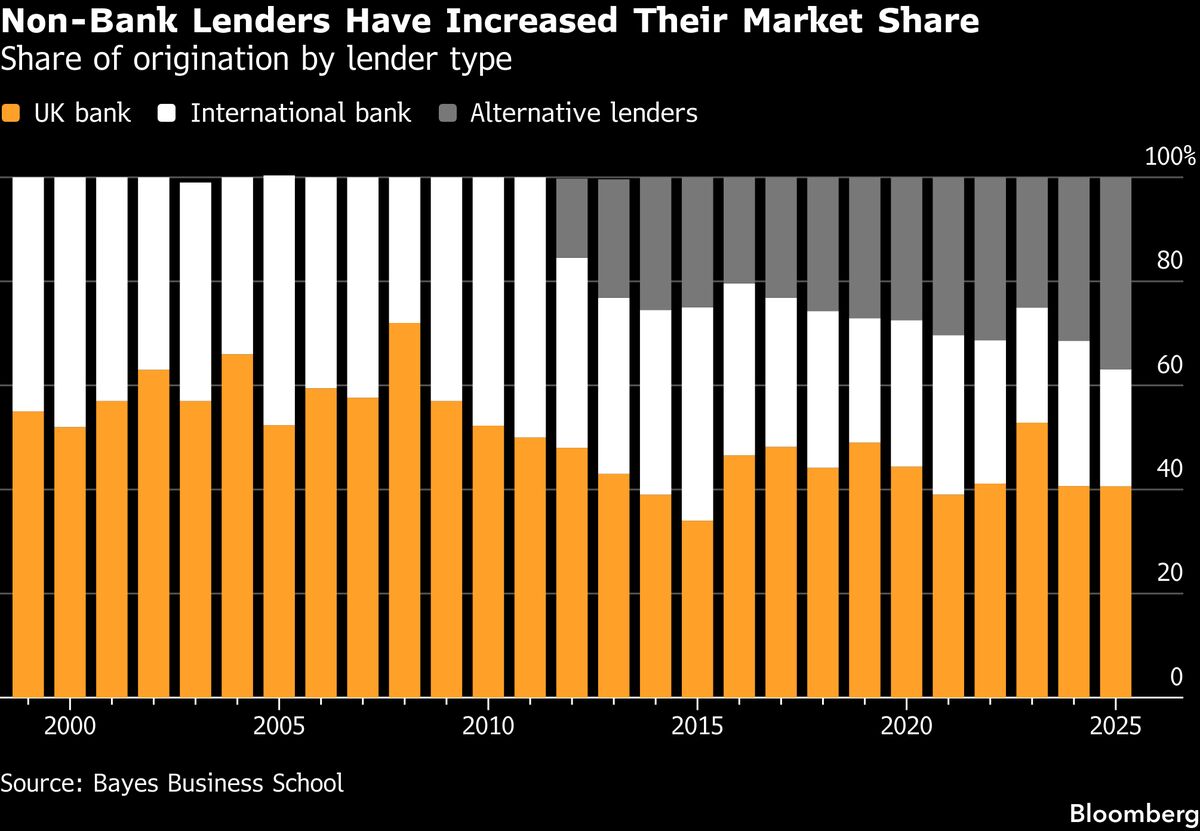

London, UK – In a seismic shift reshaping the UK’s real estate finance landscape, debt funds have more than doubled their market share over the past five years, capitalizing on banks’ retreat from direct lending under the weight of post-crisis regulations. Once the dominant force in property financing, traditional lenders have ceded significant ground to alternative financiers, with debt funds now accounting for nearly a third of all real estate loans—up from just 15% in 2018. This dramatic reallocation underscores how regulatory constraints, evolving investor appetites, and a hunger for higher yields are redrawing the boundaries of commercial real estate finance.

The Rise of Debt Funds: Filling the Void Left by Banks

The UK property market, long reliant on bank financing, has undergone a quiet revolution. According to industry analyses, debt funds—typically backed by institutional investors such as pension funds, private equity firms, and insurance companies—have surged to fill the gap left by risk-averse banks. Stricter capital requirements imposed after the 2008 financial crisis, including Basel III rules, have forced banks to reduce exposure to long-term, illiquid assets like commercial real estate loans. Meanwhile, debt funds, unencumbered by the same regulatory burdens, have aggressively expanded their portfolios, offering flexible terms and higher leverage to developers and landlords.

“Banks are no longer the only game in town,” said Marcus Harrington, a director at real estate consultancy Knight Frank. “Debt funds have stepped in with speed and creativity, financing deals that traditional lenders would either reject or take months to approve.”

Why Investors Are Flocking to Real Estate Debt

The appeal for investors is clear: real estate debt offers attractive risk-adjusted returns in a low-yield environment. With bond markets volatile and central banks maintaining elevated interest rates, institutional capital has poured into private credit strategies, including real estate lending. Debt funds typically target annual returns between 8% and 12%, far exceeding those of government bonds or even many equity investments.

“In an era of economic uncertainty, real estate debt provides a defensive play with steady cash flows,” noted Priya Shah, head of European credit strategies at BlackRock. “Investors are drawn to the security of asset-backed lending, where loans are secured against bricks and mortar.”

The trend is not unique to the UK. Across Europe and North America, private debt funds have proliferated, but Britain’s market has seen particularly rapid growth due to its deep liquidity, transparent legal system, and high demand for development finance post-Brexit.

Regulatory Pressures and Bank Retreat

Banks’ withdrawal from direct lending has been a deliberate, if reluctant, strategy. Post-2008 reforms mandated higher capital buffers for riskier loans, making long-term real estate financing less profitable. Additionally, the Bank of England’s stress tests have incentivized lenders to prioritize short-term, low-risk assets.

“The regulatory environment has fundamentally altered banks’ risk calculus,” explained David Langton, a former HSBC executive now advising fintech lenders. “Where they once dominated development finance and large-scale commercial loans, many now prefer syndicated lending or mezzanine debt to reduce balance sheet exposure.”

This retreat has created opportunities for non-bank lenders. Private debt funds, often structured as closed-end vehicles, can take on higher leverage and longer maturities without facing the same regulatory scrutiny. Their rise has also spurred innovation, with funds offering bespoke solutions such as bridge financing, stretch senior loans, and even rescue capital for distressed assets.

Risks and Challenges Ahead

Despite their growing dominance, debt funds are not without risks. Critics warn that the sector’s rapid expansion could lead to underpriced risk, particularly if economic conditions deteriorate. The UK commercial property market has shown signs of strain, with office valuations declining due to hybrid work trends and retail assets struggling amid e-commerce growth. A sharp downturn could test the resilience of highly leveraged loans.

“The danger is that some funds are underestimating the cyclicality of real estate,” cautioned Richard Vaux, a partner at law firm Clifford Chance. “If vacancy rates rise or rental incomes fall, we could see a wave of defaults, especially in secondary markets.”

Moreover, the lack of standardized reporting in private debt markets makes it harder to assess systemic risks. Unlike banks, which disclose loan performance quarterly, many debt funds operate with limited transparency.

The Future of UK Real Estate Finance

Looking ahead, analysts expect debt funds to consolidate their position, particularly in niche sectors like build-to-rent, student housing, and life sciences real estate. Some predict they could capture 40% of the lending market within the next five years. However, competition is intensifying, with insurance companies and even sovereign wealth funds entering the fray.

Banks, meanwhile, are unlikely to reclaim their former dominance. While they remain key players in syndicated lending and interest-rate hedging, their role in direct property finance has permanently diminished.

“The market has bifurcated,” said Harrington. “Banks will focus on low-risk, relationship-driven lending, while debt funds and other alternative lenders take on the complex, higher-margin deals.”

As the lines between traditional and alternative finance blur, one thing is certain: the UK’s real estate lending landscape will never be the same. Whether this shift leads to greater stability or hidden vulnerabilities, only time will tell.